BASIC TEAM

Getting home loan is very BASIC now

Get a loan in under 5 mins

Buying a bank auction property can be an excellent opportunity to acquire real estate at a lower price than the market rate. However, it comes with its risks and challenges. Understanding the process, financing options and potential pitfalls can help you make an informed decision. Exploring the latest bank auction properties can create more valuable real estate opportunities for investors and homebuyers. So, if you’re planning to buy a bank auction property, this guide will help you understand how to purchase a bank auction property along with its benefits and risks.

Table of Contents

A bank auction property is a property seized by a bank due to the owner’s failure to repay a loan. These properties are sold through public auctions, and hence the name bank auction property. Banks aim to recover the outstanding loan amount, so they auction these properties at reduced rates. This makes such properties a popular choice for buyers and investors.

If you want to buy a bank auction property in India, it is crucial to understand process:

Step 1: Locate Bank Auction Property Listings

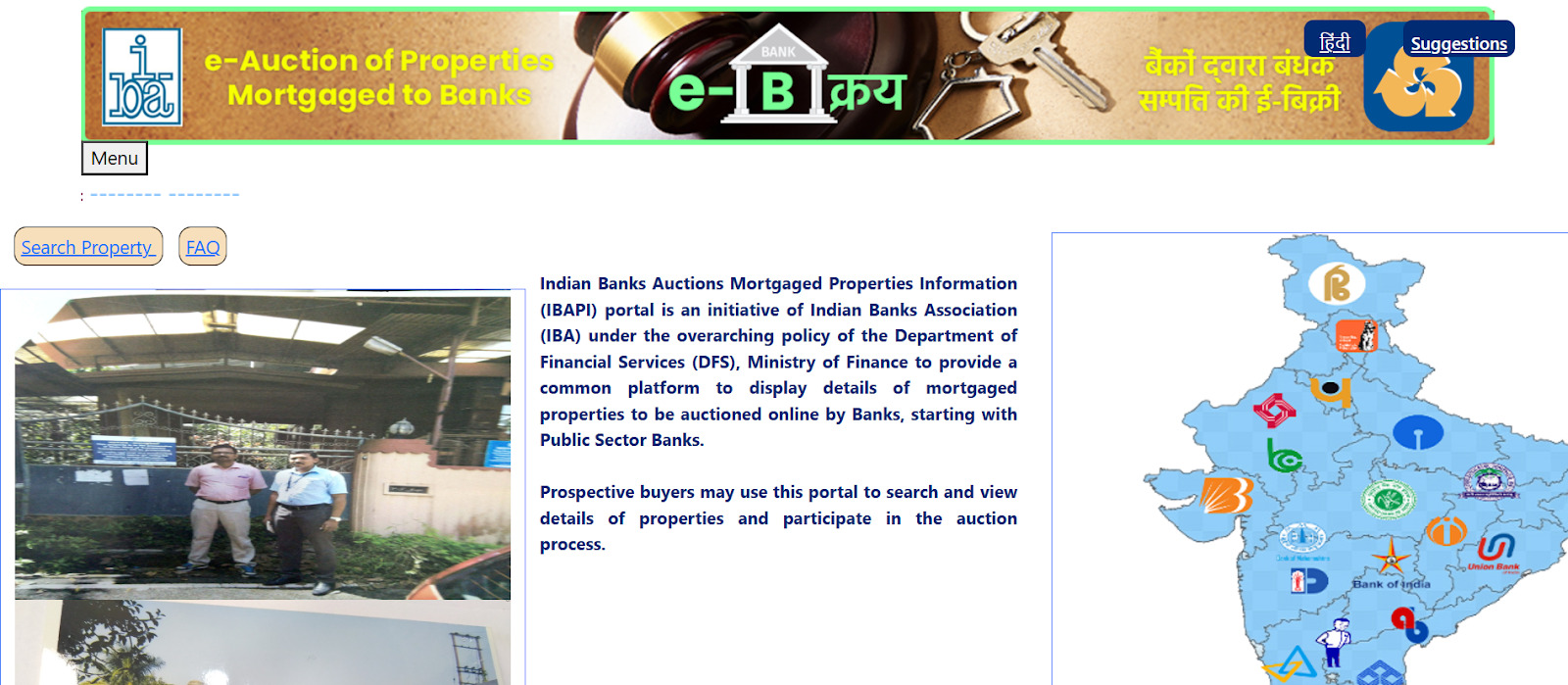

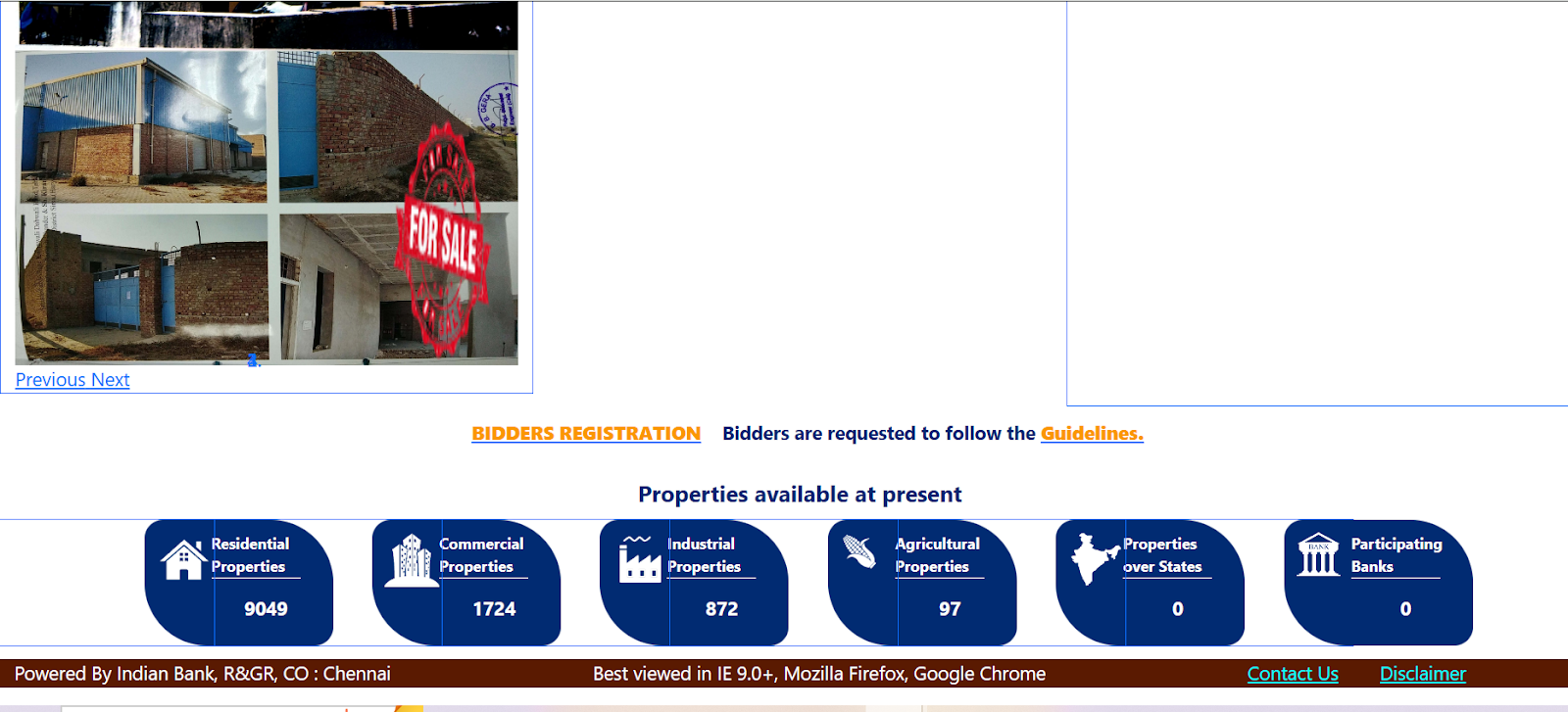

Visit the Indian Banks Auction Mortgaged Properties Information (IBAPI) portal to check the latest bank auction property listings. Here, you can find details of all the mortgaged properties available for sale via online auction by banks.

Step 2: Conduct thorough Inspections

Conduct a preliminary check after selecting a bank auction property. Verify any legal disputes, outstanding dues, or other property-related issues before participating in the auction. You are also advised to do a thorough physical inspection of the property on the dates mentioned in the e-auction notice.

Step 3: Submit a Tender Form and Deposit the EMD

The next step is to submit the tender form along with the Earnest Money Deposit (EMD). The EMD is usually deposited via demand draft or cheque. Make sure to cross-check the information you fill in on the tender form before submitting it within the deadline. Submit the required KYC documents to complete your paperwork for the bank auction.

Step 4: Participate in the Bidding Process

You can now proceed in the bidding process through various methods. The easiest way is through a bid form. However, if you wish to submit several bids, then make sure to submit different bid forms for each bid. Some banks require physical bid forms and a separate online bid form for the bidding process. In an e-auction, bidders can place multiple bids, as there is no fixed procedure.

Step 5: Review Auction Results on the Designated Date

Banks open all the qualified bids in front of the bidders on a designated date. You can check this auction result online, or by visiting the bank or the auction location on the auction result day. Winning bidders must deposit 25% of the bid amount within 24 hours. The remaining 75% must be paid within 15 to 30 days of the auction. The best way to arrange for finances to pay this deposit is through home loans.

Step 6: Register the Sale Certificate at the Sub-Registrar’s Office

The buyer receives a sale certificate after paying the remaining 75%. The title transfer will be done once the sale certificate is registered at the sub-registrar office. Make sure to check that the authorized bank executive also signs the sale certificate during property registration.

Suggested read: Home Loans for Bank Employees

Participating in a bank e-auction is a simple procedure.

Step 1: Visit the official website of the bank in whose e-auction you want to participate.

Step 2: Register as a bidder on the chosen bank property auction website.

Step 3: Once registered, accept the terms and conditions and follow the instructions to participate in bidding for a bank e-auction property.

Here are the main reasons why people show interest in investing in a bank auction property:

Suggested read: Choose Best Bank for Home Loan

It is equally important to understand the risks associated with bank auction properties before you make the final call.

The e-auction of properties mortgaged to banks offers investors and homebuyers a unique opportunity to buy real estate at a competitive price. Although the process of buying bank auction properties may seem complex, thorough research, due diligence, and financial preparedness can help you secure a great deal. With the right approach, patience, and strategic bidding, you can turn a bank auction property into a valuable asset.

To take possession of a bank auction property, you must:

Pay the full bid amount

Get the sale certificate

Register the property at the sub-registrar office

Yes, you can get a home loan for a bank auction property. However, approval depends on legal clearance, eligibility criteria, and document verification.

You can participate in the SBI property auction by registering on the SBI e-auction portal. Once registered, you must submit the KYC documents, pay the EMD, and then place the bid online on the auction date.

If a borrower fails to repay the loan, then the bank can take possession of a property after issuing a 60-day demand notice under the SARFAESI Act, 2002.

The reserve price in an auction is the minimum bid amount set by the bank or the seller. This price is based on property valuation and bids below this price are not valid.

Published on 25th March 2025

Get a loan in under 5 mins