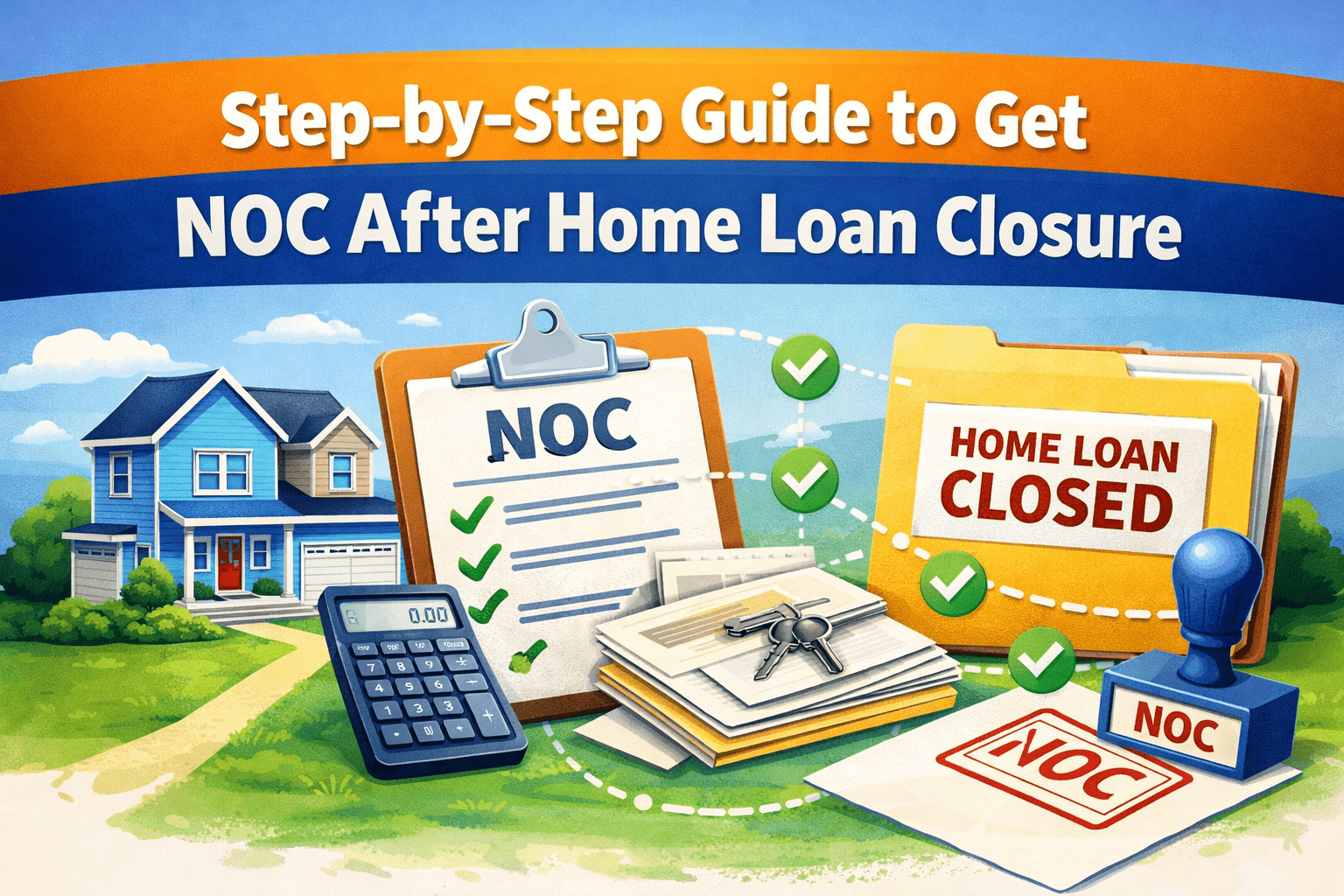

Declaring a home loan in the income tax return is less about “informing” the department and more about correctly reporting income from house property and claiming eligible deductions using the right schedules and supporting documents. When done properly, it reduces taxable income in a legally defensible way and prevents common mismatches between Form 16, ITR, […]